Every now and then, the investors find themselves scratching their heads. When they look at a big conglomerate, say, a giant corporation that makes everything from soap to software, and wonder why its stock market value seems lower than the sum of its parts.

This isn’t a mathematical mistake. It’s a phenomenon known as the “conglomerate discount.” Markets, for many reasons, tend to undervalue large, diversified groups. But interestingly, when one of these giants decides to break itself up, often by spinning off a subsidiary into an independent company, suddenly, hidden value emerges, and shareholders are rewarded.

Why does this happen? Why does a company worth $100 billion as one entity suddenly become worth $120 billion when split into two? Let’s break it down with real-world stories, in layman’s terms.

The Conglomerate Discount

When a company owns too many unrelated businesses, investors often apply a “discount.” They assume management’s attention is divided, the good businesses are being dragged down by weaker ones, and the overall complexity makes it hard to understand the company’s true worth. Studies have consistently shown that diversified companies trade at 13-15% discounts compared to focused, pure-play companies in the same industries.

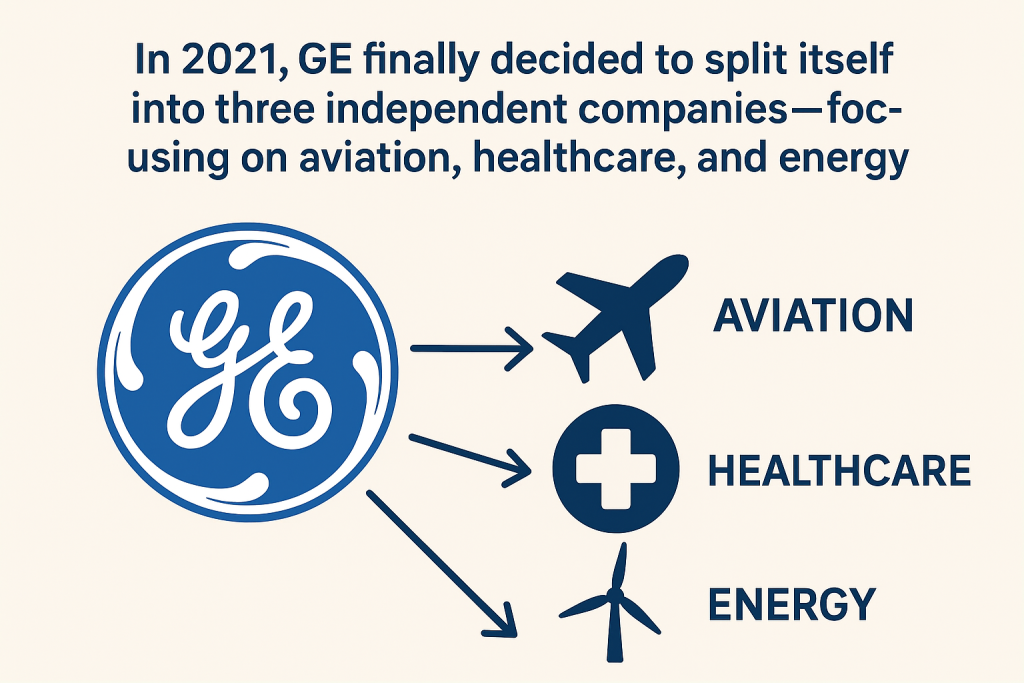

Classic Example: General Electric (GE)

For decades, GE was an example of a global conglomerate. It made jet engines, ran a massive finance arm, manufactured appliances, and even owned a TV network (NBC). But over time, GE expanded so much that the analysts struggled to value it. The whole became worth less than the sum of the parts.

In 2021, GE finally decided to split itself into three independent companies—focusing on aviation, healthcare, and energy. The decision was widely seen as an attempt to unlock the hidden value trapped within the conglomerate structure.

Why Conglomerates Exist in the First Place

In the mid-20th century, especially the 1960s and 70s, the conglomerate boom was in full swing. CEOs believed diversification was a shield: if one sector suffered, another would flourish.

Like ITC in India, which started as a tobacco company but later expanded into hotels, packaged foods, stationery, and even IT services. The idea was simple: multiple streams of income = less risk. But what worked decades, no longer convinces modern investors, who prefer focused, “pure-play” companies.

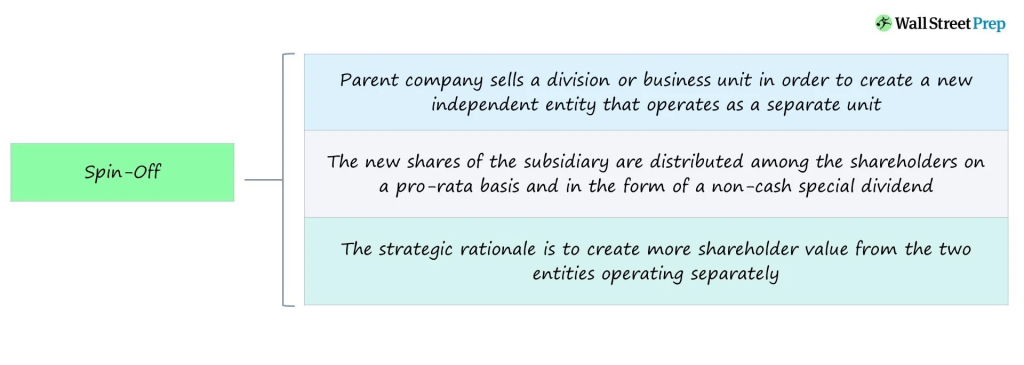

Spin-Offs: The Magic Trick to Unlock Hidden Value

A spin-off happens when a parent company separates one of its divisions into a new, independent, publicly traded company. Shareholders of the parent company typically receive shares in the new entity. Like if you own 100 shares of the parent company before a spin-off, you might end up with 100 shares of the original company plus 50 shares of the newly independent subsidiary. You haven’t spent any additional money, but you now own two focused companies instead of one.

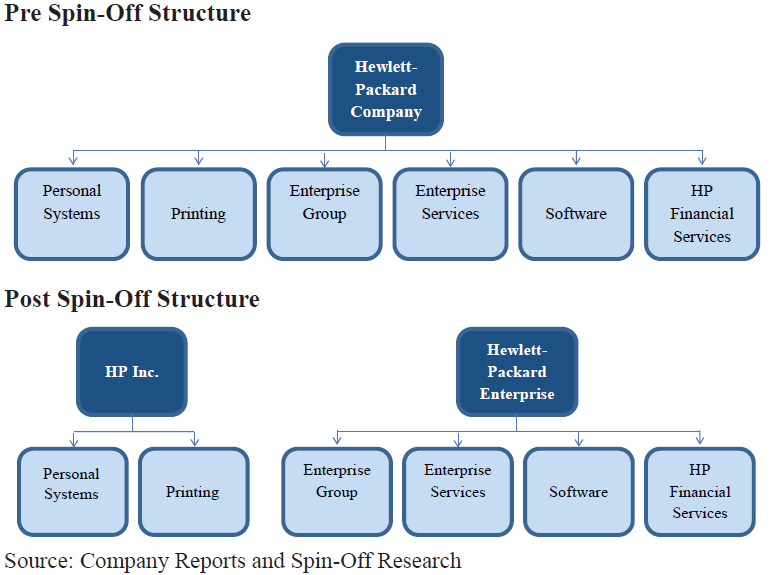

The HP Story: One Giant, Two Stronger Independents

Back in the early 2010s, Hewlett-Packard (HP) was struggling. The company had grown into a huge tech conglomerate selling everything from PCs and printers to high-end enterprise servers, software, and IT services. On paper, HP was still massive, annual revenues of over $100 billion. But investors weren’t impressed.

- The PC and printer business was slow-growing, highly competitive, and tied to consumer spending cycles.

- The enterprise hardware and services business catered to big corporations, requiring a very different strategy and investment style.

The market applied a conglomerate discount and pushed its stock prices down. In 2015, HP made a bold move. It announced it would split into two independent companies:

- HP Inc.: focusing on personal computers and printers.

- Hewlett-Packard Enterprise (HPE): focusing on servers, storage, cloud solutions, and enterprise services.

The logic was simple: each business could pursue its own strategy without being weighed down by the other. Post the split, both companies attracted their natural investors, proving how breaking up a conglomerate can transform “confused value” into stronger, more visible worth.

Why Spin-Offs Work: Three Human Reasons

1. Clarity

Investors prefer simplicity. A company that does one thing really well is easier to understand, analyse, and value. When PayPal separated from eBay, analysts could finally judge it on its own merits, without the noise of eBay’s slower marketplace business.

2. Focus

Management teams in spin-offs are no longer competing for attention within a giant corporation. Suddenly, they have the independence to make bold decisions. For example, Fiat Chrysler spun off Ferrari in 2016. As a separate entity, Ferrari could pursue its luxury branding without being tied to the mass-marketing strategies of Fiat.

3. Unlocking Investor Appetite

Certain investors prefer certain types of businesses. Some want high-growth tech stocks, while others like stable, dividend-paying companies. When a conglomerate splits, each new company attracts its “natural” investor base, boosting valuations.

The Flip Side of Spin-Offs: When Freedom Doesn’t Mean Success

Sometimes, spin-offs simply expose a business’s weaknesses instead of unlocking hidden strengths. Like AOL, which turned from an internet sensation to a spin-off struggling.

Back in the 1990s, millions of Americans logged in using AOL’s dial-up service, with that iconic “You’ve Got Mail” notification. At its peak, AOL was valued higher than some of the world’s biggest companies.

But technology moves tremendously fast. By the 2000s, broadband internet made dial-up obsolete. AOL’s business was fading. In 2001, it merged with media giant Time Warner. The idea was to combine old-school media with the new internet frontier. Instead, it turned into a disaster, cultures clashed, strategies failed, and AOL lost its relevance. By 2009, Time Warner had had enough, and it decided to spin off AOL as an independent company.

In this case, the spin-off was more like removing a crutch than unlocking potential. Eventually, AOL was sold to Verizon in 2015 for around $4.4 billion, a far cry from its glory days.

Conclusion

Conglomerates will always exist, and so will conglomerate discounts. Some will break apart to unlock value; others, like Berkshire, will thrive as unified giants. Spin-offs, meanwhile, will continue to fascinate investors as one of the simplest ways to reveal hidden worth.

In the end, the stock market is less about numbers and more about stories. A spin-off tells a new story, one of independence, focus, and clarity. And investors, like all humans, are willing to pay more for a story they can finally understand.

{kind=link}