Introduction

In 2003, Ashok Kapoor, Rana Kapoor, and Harkirat Singh proposed opening a private sector bank named YES BANK to the RBI (Reserve Bank of India). After securing all the necessary permissions and completing the paperwork, YES BANK opened its first branch in Mumbai in 2004.

The bank was a huge success. Seeing this success, within a year, YES BANK launched its IPO (Initial Public Offer) in 2005 and raised ₹315 crore from the market.

YES BANK was operating in three banking forms:

- Retail Banking – Banks that accept deposits, manage money, and lend loans to the general public.

- Corporate Banking – Banks that accept deposits, manage money, and lend loans to large corporations and businesses.

- Investment Banking – Banks that provide investment advice and manage corporate funds.

But while YES BANK saw initial success, let’s take a look at what went wrong

The YES BANK Crisis, 2019

In 2019, YES BANK faced a major issue in its balance sheet, the rapid growth of Gross and Net NPAs (Non-Performing Assets). This was a serious concern because, in banking, the biggest assets are the loans given to the public and corporations. If large corporations fail to repay their loans, it puts both the bank and its depositors at risk.

YES BANK tried its best to control the NPAs by easing repayment terms and restructuring loans, but nothing worked. Since YES BANK was a listed company, under SEBI guidelines, it had to share its financial reports with the public.

This triggered the bank’s worst nightmare, and a large portion of depositors began withdrawing their money. This massive withdrawal drained liquidity from YES BANK’s system, and if all liquidity were to be exhausted, the bank would collapse.

RBI to the Rescue

To prevent the collapse, the RBI (Reserve Bank of India) decided to intervene and took five major steps:

- Moratorium Imposed (5 March 2020)

RBI placed a withdrawal limit of ₹50,000 per depositor to slow down the outflow of funds from YES BANK. - Capital Infusion

Using its authority, RBI directed SBI to purchase a minimum of 26% stake in YES BANK and advised other banks to infuse capital. - Equity Dilution (Bail-in Mechanism)

Share capital was written down, meaning shareholders had to bear losses. AT-1 bonds were written off, making them worthless for investors holding those bonds. - Change in Management

The previous board was dissolved, and a new board was appointed with Prashant Kumar (ex-SBI) as MD & CEO. - Operational Revival

On 18 March 2020, the moratorium was lifted and normal banking operations resumed. The focus shifted to reducing losses, cleaning up the balance sheet, and improving asset quality.

Changes In the Accounts after this

Let’s see what changes have happened after the reconstruction in the financial books & market.

1) Yes Bank Equity Capital Reduction & Restructuring

| Particulars | Before Reconstruction | After Reconstruction | Notes |

|---|---|---|---|

| Face Value of Shares | ₹2 per share | ₹2 per share (unchanged) | No change in face value |

| Paid-up Equity Capital | ~₹1,250 crore | ~₹1,250 crore (but diluted in % holding) | Investors lost their entire value |

| AT-1 Bonds | ₹8,415 crore outstanding | Written off completely | Investors lost entire value |

| Shareholding (Promoters, Public, FIIs, etc.) | 100% (existing investors) | Diluted after SBI & others invested | Ownership diluted drastically |

| SBI Holding | 0% | 48.21% (initially) | Existing capital is not written off, but diluted |

| Other Banks (ICICI, Axis, HDFC, Kotak, Federal Bank, etc.) | 0% | ~20% combined | Participated in capital infusion |

| Public & Others (after dilution) | 100% | ~30–32% | Equity diluted due to new infusion |

2) Yes Bank – Writing off Losses (2020)

| Particulars | Amount (₹ crore) | Treatment/Adjustment |

|---|---|---|

| Gross NPAs (2019–20 peak) | ~32,878 | Large portion written off / restructured |

| Net NPAs | ~8,627 | Adjusted against provisions & capital |

| AT-1 Bonds Outstanding | 8,415 | Written off fully (loss to bondholders) |

| Accumulated Losses (FY20) | ~16,418 | Adjusted against reserves & fresh capital |

| Deferred Tax Assets (DTA) | 1,272 | Partially written down |

| Equity Capital | 1,250 | Not reduced in face value, but shareholder wealth eroded due to dilution |

| Fresh Capital Infusion (SBI + Others) | 10,000+ | Used to cover losses & restore CRAR (Capital Adequacy Ratio) |

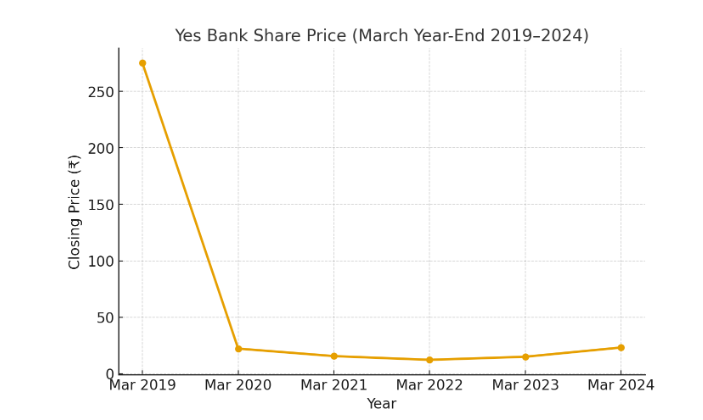

3) Equity Share prices

| Year | Closing Price (₹) |

|---|---|

| March 2019 | 275.10 |

| March 2020 | 22.24 |

| March 2021 | 15.60 |

| March 2022 | 12.30 |

| March 2023 | 15.05 |

| March 2024 | 23.20 |

Conclusion

In conclusion, when you are conducting a business like banking, which is directly connected with the economy of a nation, every decision is important. One mistake can cost the lives and finances of millions. By studying this case study, it has been shown that there is still some work to do in the field of banking security. On the other hand, it also shows the determination of the Central Bank of India, which is the RBI, to save private sector banks for the betterment of society.

{kind=link}