What comes to your mind when you’re about to hit that “Buy Now” option while purchasing something in an e-commerce store online? For many shoppers these days, it’s not just about the product—it’s about how to pay for the product. Increasingly, the choice isn’t between a credit card or debit card, but whether to use a Buy Now, Pay Later (BNPL) option. With just a click, the ₹1,000 you planned to spend can be split into four small payments over six weeks, with no interest added.

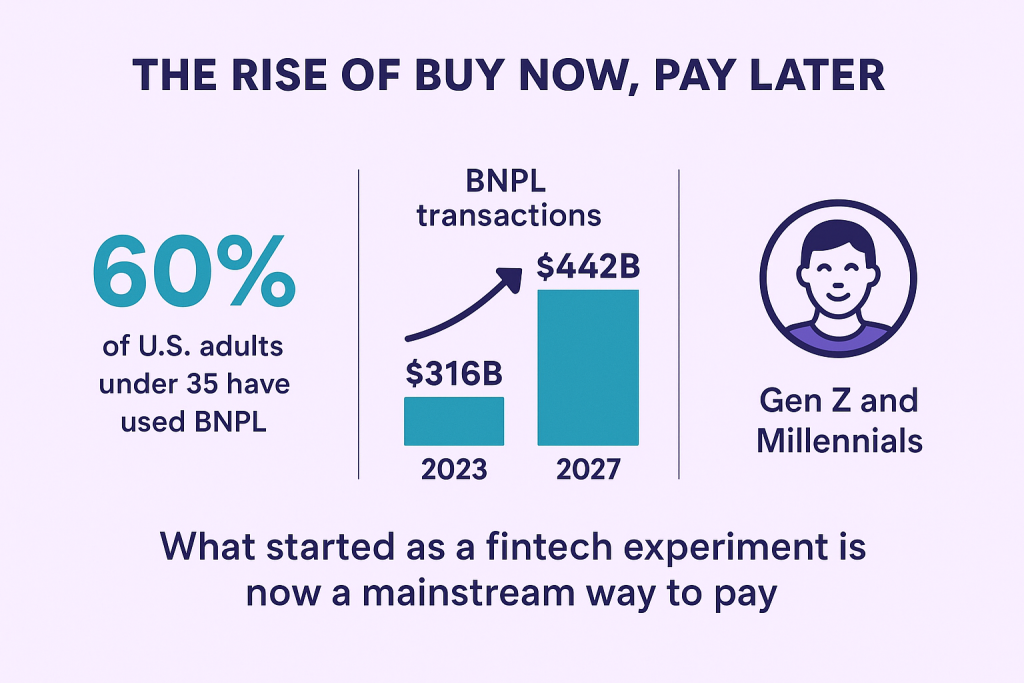

This simple option of Buy Now, Pay Later, has changed the way millions of people purchase online. A 2024 survey found that over 60% of U.S. adults under the age of 35 had used the BNPL option at least once in their lives while purchasing. Globally, BNPL transactions had reached $316 billion in 2023 and are projected to hit $442 billion by 2027. What in the beginning started as a fintech experiment is now a mainstream way to pay, especially for Gen Z and Millennials, who are cautious about credit card debt.

But here’s where the bigger question comes: if consumers aren’t paying interest, who is paying for this convenience? The truth is that BNPL isn’t “free.” The costs are hidden in higher fees for merchants, in the borrowing expenses carried by providers, and in the risks of customers missing payments. Let’s decode the process even better in this article.

How do BNPL transactions actually work?

At first glance, BNPL looks very simple: you buy something today and pay the worth of the product later in equal installments for a fixed period. But behind that one click, there’s a whole chain of events happening.

For instance, you purchase a mobile phone worth ₹10,000 on an e-commerce website. The BNPL company immediately pays the merchant the full amount minus 2-5% of commission. Later, as per your agreement to pay back the BNP provider in small installments, with a minimal fee as a processing fee if prescribed from case to case.

So while the customer feels it is “free,” the cost is carried by the merchant and indirectly by all shoppers through slightly higher prices.

BNPL Wave in India

In India, BNPL is growing promptly because of its convenience to shoppers. As per the latest report, only 5% or fewer people in India have access to credit cards, while over 350 million people shop online. Here comes BNPL, filling this gap by offering instant, small-ticket value loans with minimum paperwork.

The Indian BNPL sector was valued at $5 billion in 2022 and is expected to cross $50 billion by 2026, growing at a stagnant rate of 60–70% every year. This makes India one of the fastest-growing BNPL markets in the world.

Several companies are leading this space. Among them, ZestMoney is quite popular for higher-valued purchases like electronics or furniture, while Simpl and LazyPay are widely used for everyday/frequent purchase needs such as food delivery, groceries, and utility bills. To catch this phenomenon, e-commerce giants have also stepped in, like Amazon Pay Later and Flipkart Pay Later, which make checkout faster and smoother. Paytm Postpaid has expanded BNPL even further into recharges, bill payments, and travel bookings.

For students and young workers, BNPL feels like freedom—it gives them the power and convenience to purchase more and rely on buying now and worrying later, but this freedom comes with its cost.

With strong demand and multiple players in the market, BNPL is no longer just a trend—it is fast becoming a normal way to pay in India. Experts believe that in the future, BNPL may even merge with UPI, which could bring instant credit to millions more people.

Operational Model of BNPL

Ever wondered if the Buy Now, Pay Later option isn’t charging you any interest, how do BNPL companies survive and make money? The reality is, there is nothing “free” in the process. The firms earn their money actively from different sources.

The first and biggest source of income is merchant fees. Every time a shopper uses BNPL at the checkout section, the seller pays the BNPL company a commission—usually this is between 2-5% of the purchase value. For a better comparison, traditional credit card networks like Visa or Mastercard usually charge merchants between 1–2%.

Sellers are willing to pay this higher fee because BNPL attracts shoppers and increases sales. In fact, studies show that offering BNPL at checkout can boost sales by 20–30%.

But this ease comes with risks of default. Many shoppers miss payments knowingly and unknowingly. These defaults directly hurt the company, as they have already paid the merchant full price. To soften this loss, BNPL firms charge late payment fees—usually a smaller portion of the amount—which form an important part of their income.

Another big factor is funding costs. When you buy something using BNPL, the merchant is paid immediately. However, the BNPL company has to wait to recover money back in installments. To cover this period, they borrow money from banks or raise funds from investors. Borrowing or raising funds comes with the cost of interest, or a dividend, which eats into company profits. This is the sole reason why many BNPL companies, even the big global ones, still struggle to become profitable despite their popularity.

So while BNPL looks “interest-free” to the shopper, the costs are spread across merchants, late fees, and the borrowing expenses carried by the providers.

The Risk Factor to Shoppers

BNPL comes with the ease of a credit card but often carries higher risks. The first is an increase in overspending habits. Since payments are broken into smaller portions, shoppers feel less burdened and end up buying more than they really need. What looks like a simple purchase often turns into a habit of spending.

The second risk is the debt trap, because installments keep running one after another, resulting in constantly juggling for money, resulting in multiple BNPL loans at the same time. This cycle of continuous repayments makes it even more difficult to stay debt-free.

Another challenge is late fees. Missing even one installment can lead to extra charges of a late fee, which may look like a smaller portion in the beginning, but as time passes, it becomes a pile.

There is also a risk of a low credit score. Yes, even though BNPL is a credit card-free option, it affects shoppers’ credit ratings. BNPL records are now reported to credit bureaus; even a small delay or default can lower CIBIL score/credit score, which affects chances of getting bigger loans in the future.

Regulators Landscape

In India, the Reserve Bank of India (RBI) had instructed fintech companies to stop loading credit lines onto wallets and prepaid cards, which forced many BNPL providers to pause or redesign their services in the year 2022 because of no strict rules between BNPL and its intermediaries and shoppers.

The same concerns are seen worldwide. In the United States, the Consumer Financial Protection Bureau (CFPB) is reviewing BNPL and moving toward classifying it as a form of credit. This means providers will have to share clearer terms, charges, and risks with customers. In Europe, countries like the U.K. and Germany are also working on stronger regulations for proper and effective use.

The Future of BNPL

BNPL is not likely to disappear soon; in India, it may grow even faster than in other countries. The reasons are clear: India has one of the largest groups, and yet less than 5% of Indians own credit cards. In the coming years, BNPL could even merge with UPI offerings, resulting in instant credit available to millions of people.

What started as a simple “buy now, pay later” button is now going to become a global shift in how people use credit. If used wisely, it can be a helpful tool. Used carelessly, it can quietly turn into a burden.

Disclaimer: This article is meant for general information and educational purposes only. It does not provide financial or legal advice. Readers should carefully check the terms and conditions of BNPL services and consult a qualified financial advisor before making borrowing or repayment decisions.

{kind=link}